What is an IVA?

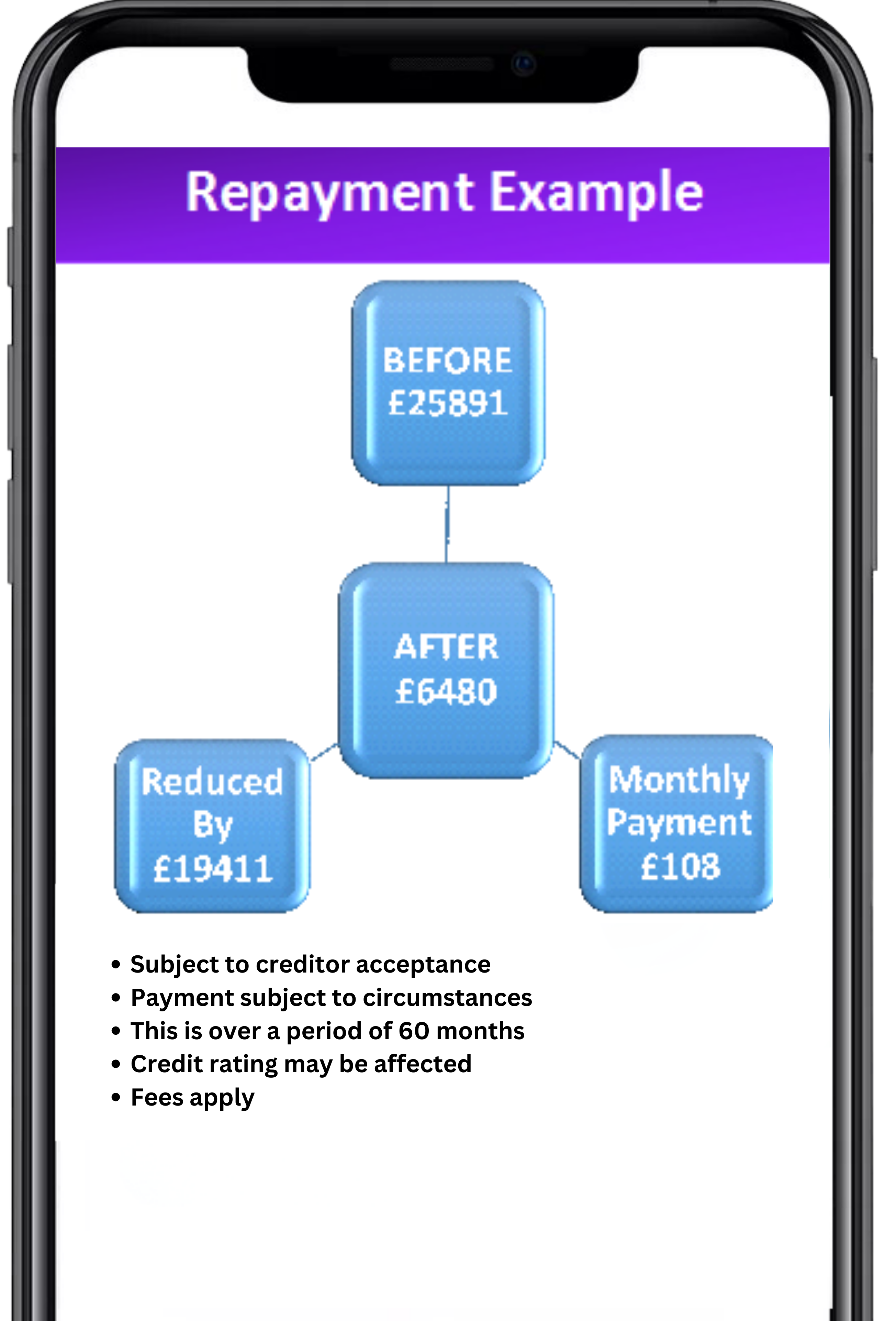

An individual voluntary arrangement (IVA) is a formal agreement allowing you to make affordable payments to your debts, usually over five or six years. At the end of your IVA any unsecured debt left is written off. You can also make a one-off payment known as a lump-sum IVA. You can expect to write off up to 85% of your unsecured personal debts with an IVA. The amount of debt that you can write off with your IVA will depend on what you can afford to pay.

Your creditors cannot demand any additional payments from you unless your financial circumstances improve during the life of the IVA. During the IVA, the creditors are legally bound to freeze the interest on any outstanding debts and to cease adding late payment charges to the debtor’s accounts. Once an IVA has been successfully completed any outstanding balances must be written off by the creditors, in many cases as much as 85% leaving the debtor debt free. If you are a homeowner, you may need to release equity from the value of your home. If no remortgage is available, the IVA may be extended for 12 months.

Whether you qualify for an IVA depends on how much you owe, what assets you have, what you can afford to pay into the IVA and the stability of your income to enable you to maintain payments.

Is an Individual Voluntary Arrangement right for you?

To qualify for an IVA you must have more than one unsecured debt, such as a personal loan, credit card or overdraft. You must also have a disposable income to pay towards your debts.

A number of debts can be included on an IVA with the exceptions of student loans, court fines, child maintenance arrears and secured debts, although other exclusions may apply.

IVAs are not available in Scotland – Protected Trust Deeds are an alternative to IVAs in Scotland. An IVA proposal is a legal document, so the applicant must provide suitable evidence to support the proposal, such as payslips and bank statements.

As a formal insolvency procedure, an IVA is a legally binding agreement with your unsecured creditors and requires an Insolvency Practitioner. There are fees involved, but these do not impact on your payment, which will always be calculated as an amount affordable to you.

Benefits of an Individual Voluntary Arrangement (IVA)

Once your IVA is approved by your creditors you will make one affordable monthly repayment, for a set period and have a countdown to clearing your debt.

If the IVA is approved, interest and charges are guaranteed to be frozen

You will stop receiving letters and phone calls from your creditors and debt collectors chasing you for payment.

Any legal action against you in respect of recovering the debts, such as bailiffs, will stop.

If you are a homeowner, your house will be protected.

Making one regular monthly payment allows you better control over the rest of your finances.

If you have a debt in joint names with someone else, this can be included in your IVA. However, your creditors may still chase the other person for all of the debt.

The outstanding balance of unsecured debts included within the IVA will be written-off at the end.

If you have a lump sum to offer, this can be paid as a one-off ‘full and final’ settlement, or a combination of monthly payments followed by a lump sum payment.

Debts Included in an IVA

An IVA would cover most of your unsecured debts. Debts covered by IVA include:

- Overdrafts

- Personal loans and catalog debts

- Council Tax arrears

- Hire-purchase debts

- Credit and store cards

- Money owed to HMRC, e-g income tax (unless fraudulent)

- Water bill arrears

- Benefit overpayments

- Payday loans

- Joint debts, but the other person must also make payments

- Tax credit

- National insurance arrears

Debts Not Included in an IVA

An IVA does not cover most secured loans. Debts not covered by an IVA include:

- Mortgages

- Student loans

- Social fund loans

- Court fines

- Child maintenance or child support dues

- TV license arrears

- Hire-purchase agreements

- Debts accumulated through fraudulent conduct

- Certain forms of car finances

- Other secured debts

Potential drawbacks of an Individual Voluntary Arrangement (IVA)

To ensure the repayments are fair to you and your creditors, there are restrictions on expenditure when in an IVA. If you have a windfall, such as inheritance or a lottery win, you will need to pay a proportion of this into the IVA.

Lenders are not obliged to accept your IVA and you are at risk of Bankruptcy if your IVA fails.

The IVA will appear on your credit file for 6 years. Details of your IVA will appear on the Individual Insolvency Register. Secured debts including charging order will remain outstanding.